Ariad Pharmaceuticals (ARIA) and Merck (MRK) are co-developing a small molecule inhibitor of the mammalian target of rapamycin (mTOR) called ridaforolimus. ARIA announced that ridaforolimus has shown to reduce the cancer progression by 28 percent and increased progression free survival by about 3 weeks. The most frequent adverse effects were mouth sores, fatigue, diarrhea and low platelets. MRK plans to submit for FDA approval this year. ARIA's stock price jumped 30% after the announcement. ARIA has no currently approved drugs. ARIA will be eligible for milestone and royalty payments. ARIA's current stock price is nearly three times higher than one year ago.

If approved, it would be the 2nd in class drug for treatment of cancer; temsiroliums (Torisel) was approved by FDA for treatment of renal cell carcinoma and is manufactured by Wyeth, now owned by Pfizer. Torisel showed slightly better results, but it was in a different type of cancer and renal cell carcinoma is known for having mTOR dysregulation. Rapamycin is another drug in this class, but is approved for prevention of transplant rejection.

mTOR is a protein that integrates signals from insulin, growth factor, and cell division pathways. It is often dysregulated in cancers and is a potential target for treatment. It interacts with othere pathways and proteins that are involved in various forms of cancer such as the Abl gene, which is translocated and fused with Bcr in chronic myelogenous leukemia. Despite the inter-connectivity with other pathways, the adverse effects are minimal and not of great concern. This can be attributed to the specificity of the drugs. ARIA and MRK are also conducting ridaforolimus clinical trials in breast, lung, prostate, pediatric, endometrial, and other solid tumors. Most of these trials are in Phase II.

There is a huge potential for ridaforolimus and can become ubiquitous in oncology as doxorubicin. With a great tolerability profile for a cancer drug and continuing good results from clinical trials, ridaforolimus can be very profitable for ARIA and MRK. Also, investors should monitor results from clinical trials of both ridaforolimus and Torisel and compare results for the same types of cancers. These trials are generally conducted in patients who have failed other therapies, so they are in the worst condition. Results from studying ridaforolimus as a first line therapy should show better results.

Tuesday, January 18, 2011

Monday, January 10, 2011

Avanir Pharmaceuticals Looks to Treat Uncontrollable Laughing and Crying

The FDA approved a new drug for the treatment of uncontrolled laughing and crying associated with some neurological conditions such as multiple sclerosis and Lou Gehrig's disease or amyotrophic lateral sclerosis. The medication is called Nuedexta and is a product of Avanir Pharmaceuticals (Nasdaq: AVNR). It is the first approved drugs for pseudobulbar affect, in which patient cannot control their emotion. The drug has not been shown to be safe or effective in patients with other mental disorders, such as Alzheimer's and dementia. [WebMD]

Typically a stock's price increases when the company gets FDA approval, but the value of the company should be based upon the impact and market share the drugs will obtain. Neudexta should be on the market by March. Currently, I do not see Neudexta being a big time drug for several reasons and do not think that it will lead to appreciation of of Avanir's stock price. Neudexta is a good treatment for those who suffer from uncontrollable laughter or crying, but investors will not benefit from it's approval.

AVNR has no other drugs on the market. Abreva (10% docosanol cream) was granted to GSK to market in North America. AVNR has a drug candidate AVP-923 in Phase III clinical trials for the treatment of diabetic peripheral neuropathy. Two other candidates, a MIF inhibitor and Xenerex, were sold to other companies.

Neudexta is a combination of two drugs that are already on the market, quinidine and dextromethorphan (DXM). Quinidine is an anti-arrhythmic and is associated with a variety of side effects such ringing in the ear, thrombocytopenia (low platelets), granulomatous hepatitis, myasthenia gravis (an autoimmune disorder resulting in muscle fatigue and weakness), and torsades de pointes (type of arrhythmia). Because of these side effects, quinidine is rarely used. The drug was not approved in 2006 due to safety concerns of quinidine. Given the high prevalence of malpractice lawsuits, physicians will be reluctant to prescribe Neudexta for their patients. The approved formulation consists of a lower dose of quinidine to address the concern. DXM is a relatively safe drug and is found in OTC cough syrups. There are no studies about the effects of using DXM for prolonged time. Typically, patients take DXM for about a week to suppress their cough. Long term abuse of DXM has been associated with cognitive deterioration. [Journal of Psychiatry & Neuroscience]

Since these drugs are already on the market and inexpensive compared to newer chemical agents, don't expect AVNR to be able to set a high price for Neudexta. A blog on "Seeking Alpha" reports a co-pay ranging from $60-$340 for a 90 day supply.

The market for Neudexta is not huge. Don't expect AVNR to be raking in cash. It is estimated that 20,000-30,000 people in the United States have ALS. [NIH] Of those diagnosed with ALS, approximately 50% experience pseudobulbar affect. A smaller percentage of MS patients experience pseudobulbar affect (10%). [Neurology Today]

I just can't get excited about AVNR. Neudexta is not a blockbuster or even a drug that will generate considerable revenue. There's the risk of arrhythmia, which is very concerning. Besides AVP-923, AVNR has no other drug candidates in its pipeline. AVNR has a beta of 2.48, P/E of N/A, and a market cap of 517.46M. Investors should be cautious and think twice or maybe thrice before investing in AVNR.

Typically a stock's price increases when the company gets FDA approval, but the value of the company should be based upon the impact and market share the drugs will obtain. Neudexta should be on the market by March. Currently, I do not see Neudexta being a big time drug for several reasons and do not think that it will lead to appreciation of of Avanir's stock price. Neudexta is a good treatment for those who suffer from uncontrollable laughter or crying, but investors will not benefit from it's approval.

AVNR has no other drugs on the market. Abreva (10% docosanol cream) was granted to GSK to market in North America. AVNR has a drug candidate AVP-923 in Phase III clinical trials for the treatment of diabetic peripheral neuropathy. Two other candidates, a MIF inhibitor and Xenerex, were sold to other companies.

Neudexta is a combination of two drugs that are already on the market, quinidine and dextromethorphan (DXM). Quinidine is an anti-arrhythmic and is associated with a variety of side effects such ringing in the ear, thrombocytopenia (low platelets), granulomatous hepatitis, myasthenia gravis (an autoimmune disorder resulting in muscle fatigue and weakness), and torsades de pointes (type of arrhythmia). Because of these side effects, quinidine is rarely used. The drug was not approved in 2006 due to safety concerns of quinidine. Given the high prevalence of malpractice lawsuits, physicians will be reluctant to prescribe Neudexta for their patients. The approved formulation consists of a lower dose of quinidine to address the concern. DXM is a relatively safe drug and is found in OTC cough syrups. There are no studies about the effects of using DXM for prolonged time. Typically, patients take DXM for about a week to suppress their cough. Long term abuse of DXM has been associated with cognitive deterioration. [Journal of Psychiatry & Neuroscience]

Since these drugs are already on the market and inexpensive compared to newer chemical agents, don't expect AVNR to be able to set a high price for Neudexta. A blog on "Seeking Alpha" reports a co-pay ranging from $60-$340 for a 90 day supply.

The market for Neudexta is not huge. Don't expect AVNR to be raking in cash. It is estimated that 20,000-30,000 people in the United States have ALS. [NIH] Of those diagnosed with ALS, approximately 50% experience pseudobulbar affect. A smaller percentage of MS patients experience pseudobulbar affect (10%). [Neurology Today]

I just can't get excited about AVNR. Neudexta is not a blockbuster or even a drug that will generate considerable revenue. There's the risk of arrhythmia, which is very concerning. Besides AVP-923, AVNR has no other drug candidates in its pipeline. AVNR has a beta of 2.48, P/E of N/A, and a market cap of 517.46M. Investors should be cautious and think twice or maybe thrice before investing in AVNR.

Sanofi-Aventis Looking to Acquire Genzyme and Alemtuzumab

Genzyme (Nasdaq:GENZ) a biotechnology company known for developing therapies for rare disorders is being courted by Sanofi-Aventis (Nasdaq:SNY). An earlier offer of $69/share was considered too low by GENZ. GENZ is currently trading in the $71 range. The two companies are discussing a contigent value right (CVR) that could increase the offer to $80/share.[WSJ] Carl Icahn has a representative on GENZ's board and is trying to grab more seats on the board so expect GENZ to be a very tough negotiator.

Sanofi's interest in acquiring Genzyme revolves around the monoclonal antibody, alemtuzumab (Campath). Alemtuzumab is currently FDA approved for B-cell chronic lymhocytic leukemia (B-CLL) [PI] and is being investigated as a possible treatment for multiple sclerosis (MS). SNY and GENZ disagree over the potential revenue stream generated by Campath. SNY believes the annual sales could rise to $700 million, but GENZ believes the sales figures could rise to the level of $3.6 billion because of its superiority over other treatment options. The likely sales figure is somewhere in the middle, around $1.2-1.6 billion range.

The sales figure can rise if Campath is approved for multiple sclerosis, an autoimmune disorder that affects the central nervous system. There are about 2.5 million MS patients worldwide. [National MS Society]

A phase II trial enrolled 334 MS patients to compare two different doses of alemtuzumab to high dose therapy with beta interferon 1a. Alemtuzumab was given as yearly courses (1st treatment was daily infusion for 5 days; 2nd and 3rd courses were daily infusion for 3 days; 3rd course was planned but safety concerns arose and not all patients received this course). Beta interferon 1a was administered thrice weekly by a subcutaneous injection.

Patients designated to either alemtuzumab group had superior outcomes to patients in the beta interferon 1a group. At the 3 year mark,the percent of patients who had not experienced a relapse was as follows: 77% of patients in the low dose alemtuzumab; 84% of patients in the high dose alemtuzumab group; and 52% of patients assigned beta interferon 1a. Sustained disability risk was reduced by 71% in the alemtuzumab groups compared to the beta interferon 1a group.

Three percent of participants experienced low blood platelets, which may lead to increased bleeding. This condition is serious, but treatable. The phase II trial was suspended after a fatal cure of the disorder. Low platelets remains a significant concern and expect the FDA to heavily inquire safety results during review. Side effects relating to the thyroid gland were common (22.6%), but can be treated with thyroid medications. Immune suppression is another concern of alemtuzumab therapy. [NEJM]

CARE-MS1 and CARE-MS2 are phase III trials comparing low dose alemtuzumab and beta interferon 1 in treatment naive and patients with breakthrough disease, respectively. The results of the trials should be available sometime this or next year. [Medscape]

It should a good time to be a stockholder in GENZ especially if a merger deal is reached. Icahn has tried to force several companies to be bought by others in the past such as Yahoo! and it may be the same in this case. SNY's offer of $69 expires on Jan. 21 and is unlikely to be accepted by GENZ. A favorable price would be $75-80/share which would be about 5-13% higher than the current trading price. Even if a deal is not reached, Campath has a bright outlook to be increasingly used for B-CLL and should be approved for treatment of MS for which it can be the first line drug.

Sanofi's interest in acquiring Genzyme revolves around the monoclonal antibody, alemtuzumab (Campath). Alemtuzumab is currently FDA approved for B-cell chronic lymhocytic leukemia (B-CLL) [PI] and is being investigated as a possible treatment for multiple sclerosis (MS). SNY and GENZ disagree over the potential revenue stream generated by Campath. SNY believes the annual sales could rise to $700 million, but GENZ believes the sales figures could rise to the level of $3.6 billion because of its superiority over other treatment options. The likely sales figure is somewhere in the middle, around $1.2-1.6 billion range.

The sales figure can rise if Campath is approved for multiple sclerosis, an autoimmune disorder that affects the central nervous system. There are about 2.5 million MS patients worldwide. [National MS Society]

A phase II trial enrolled 334 MS patients to compare two different doses of alemtuzumab to high dose therapy with beta interferon 1a. Alemtuzumab was given as yearly courses (1st treatment was daily infusion for 5 days; 2nd and 3rd courses were daily infusion for 3 days; 3rd course was planned but safety concerns arose and not all patients received this course). Beta interferon 1a was administered thrice weekly by a subcutaneous injection.

Patients designated to either alemtuzumab group had superior outcomes to patients in the beta interferon 1a group. At the 3 year mark,the percent of patients who had not experienced a relapse was as follows: 77% of patients in the low dose alemtuzumab; 84% of patients in the high dose alemtuzumab group; and 52% of patients assigned beta interferon 1a. Sustained disability risk was reduced by 71% in the alemtuzumab groups compared to the beta interferon 1a group.

Three percent of participants experienced low blood platelets, which may lead to increased bleeding. This condition is serious, but treatable. The phase II trial was suspended after a fatal cure of the disorder. Low platelets remains a significant concern and expect the FDA to heavily inquire safety results during review. Side effects relating to the thyroid gland were common (22.6%), but can be treated with thyroid medications. Immune suppression is another concern of alemtuzumab therapy. [NEJM]

CARE-MS1 and CARE-MS2 are phase III trials comparing low dose alemtuzumab and beta interferon 1 in treatment naive and patients with breakthrough disease, respectively. The results of the trials should be available sometime this or next year. [Medscape]

It should a good time to be a stockholder in GENZ especially if a merger deal is reached. Icahn has tried to force several companies to be bought by others in the past such as Yahoo! and it may be the same in this case. SNY's offer of $69 expires on Jan. 21 and is unlikely to be accepted by GENZ. A favorable price would be $75-80/share which would be about 5-13% higher than the current trading price. Even if a deal is not reached, Campath has a bright outlook to be increasingly used for B-CLL and should be approved for treatment of MS for which it can be the first line drug.

Wednesday, January 5, 2011

The Race to Develop the Next Blockbuster: Merck and Roche Fight High Cholesterol.

Cholesteryl ester transfer protein inhibitors (CETP inhibitors) are a novel class of drugs that have the potential to revolutionize treatment of high cholesterol much like the statins (Lipitor, Zocor, and Crestor). Like other drugs in their earliest stages of development, there has been some concern and adverse effects that raised red flags. In particular, Pfizer (NYSE: PFE) discontinued the development of torcetrapib after concern of increase blood pressure. Merck (NYSE: MRK) and Roche (PINK:RHHBY) have continued to develop their respective drugs, anacetrapib and dalcetrapib. With so promise in raising good cholesterol (HDL) and reducing bad cholesterol (LDL), these drugs can be blockbusters like the statins. Since this is a new class of drugs, the risks are relatively unknown and can be the deciding factor whether or not CETP inhibitors will ever thrive.

Dalcetrapib:

Dalcetrapib:

- It is less potent than the other two drugs and concentrations reached in clinical studies are not high enough to completely inhibit CETP. This may be a good thing.

- It acts through a slightly different mechanism than the others and does not induce a complex between CETP and HDL.

- In a Phase II, placebo controlled trial, it was shown to reduce LDL by 7%, increase HDL by 34% after 4 weeks at a dose of 900 mg/day. No increase in blood pressure was reported.

- Similar results were achieved when dalcetrapib was given with pravastatin (Pravachol). Pravastatin is not widely used. A better study should have been performed using Lipitor or Crestor.

- Current studies (dal-PLAQUE and dal-OUTCOMES) will provide a better glimpse into the potential.

- Works via the same mechanism as torcetrapib by complexing CETP with HDL. This causes researchers to be more concerned about blood pressure elevation effects.

- It is much more potent than dalcetrapib. This is not necessarily a good thing. A higher potency may translate into higher risk of adverse effects.

- In a Phase I trial, anacetrapib (300 mg/day) increased HDL by a whopping 129% and lowered LDL by 38% after 28 days of treatment.

- A separate Phase I trial tested the safety of anacetrapib in helathy patients for 10 days. There was no reported increase in blood pressure.

- A recent 8 week study evaluated anacetrapib co-administered with atorvastatin (Lipitor). The HDL increase was maintained, but the LDL was lowered by 70%. No increase in blood pressure was reported.

- The DEFINE study is ongoing and will provide a better projection of anacetrapib's potential.

- High LDL and low HDL are risk factor for atherosclerosis. CETP inhibitors help in both regards.

- Defective HDL function contributes to atherosclerosis.

- CETP inhibitors may be the preferential drugs to increase HDL.

- Combination therapy with statins, niacin, and fibrates lays in the future of CETP inhibitor therapy.

- CETP inhibitors will play a big role in the treatment of common types of high cholesterol disease states, particularly patients with metabolic syndrome and type 2 diabetes.

- Further research and investigation of CETP inhibition is needed with monotherapy and combination therapy.

- It's still too early to tell the impact on stock prices for MRK and Roche, but this is one thing to monitor for the next two years as the Phase III trials will take approximately 18 months to complete and another couple of months for follow-up study.

- It is interesting to see if these drugs can help MRK and Roche recuperate from the patent cliff of 2011-2012.

Tuesday, January 4, 2011

JNJ's Sensitive Cancer Test May Bear No Fruit.

Healthcare giant Johnson and Johnson (NYSE: JNJ) has announced a partnership with Massachusetts General Hospital to develop a new test that is sensitive to detect a single cancer cell in a teaspoon of blood sample. The announcement has received a lot of attention simply because it involved cancer detection. To the public, the test may sound amazing and a giant leap to the cure of cancer. However, there are numerous, big hurdles it must overcome to be useful in treatment.

Issues Concerning the Success of JNJ's Novel Test:

Issues Concerning the Success of JNJ's Novel Test:

- Cost will be the primary concern for any novel treatment or diagnostics. This includes costs incurred by the hospital, doctor's office, and insurance companies and if they cover the costs of the test. Costs include a new instrument, supplies to perform the test, training that may be needed in performing and interpreting the tests, and many other things. The current CellSearch test cost a couple hundred thousand dollars. Patients may draw the shortest straw.

- The technology is still in early stage of development. If successful, the instrument can be expected to hit the market in a few years.

- What real clinical value lays in detecting a single cell?

- It is well known that a tumor consists of a heterogeneous cell population. Each cancer cell is different due to the high mutation rate. A single cell would not represent the tumor and metastases.

- If the patient has a solid tumor, detection of a cancer cell in the blood would mean the cancer has metastasized. Metasized tumors are extremely difficult to treat and patients often relapse. However, this is great news if detected early and no new distant tumors have formed.

- Tumors metastasize after growing to a certain size and being depleted of nutrients. This test will not give the earliest indication of cancer.

- The test requires a couple of teaspoons of blood, roughly 10 milliliters (mL). An average adult has roughly 5 liters of blood. This means that for every 1 cancer cell detected by the test, there are 499 more cancer cells circulating in the blood.

- Not all cancers metastasize via the blood. Some cancers metastasize via the lymph system such as breast cancer. The test may be of much use for these cancers.

- The test may be better for blood cancers such as leukemia and lymphoma. It just makes more sense to tailor therapy based on blood samples when the cancer is of the blood.

- It is indirect to base therapeutic decisions on presence of cancer cells in the blood. There are many reasons why cancer cells will not be present in the blood. The tumor may be in temporary remission. Also, if the chemotherapy is very effective, it may cause tumor lysis syndrome and a lot of cellular debris may be detected in the blood resulting in a false positive.

- This is a good shot at personalization of medicine, but does not hit the bull's eye. Each patient is going to have different tumor markers and respond to therapy in different ways. The patient's cancer is going to mutate in unique ways. The test needs to account for this fact. It is more of an art than science. The report in PNAS states that the antibody on the microchip was specific for epithelial cell adhesion molecule (EpCAM). I expect the final version to contain several specific antibodies for different molecular markers.

Monday, January 3, 2011

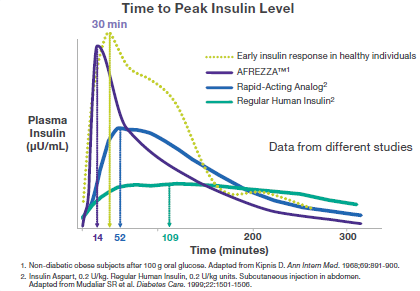

Can Mannkind Avoid Repeating History with its Inhaled Insulin, Afrezza?

Mannkind (Nasdaq: MNKD) continues to wait for FDA approval of its inhaled insulin drug candidate, Afrezza. This is not the first time an inhaled insulin formulation has come up for approval. Pfizer's (PFE) Exubera was less than exuberant. Although winning FDA approval, it was withdrawn from the US market in late 2007 after only being on the market for a year. This led to other companies to stop their development of inhaled insulin formulations. However, MNKD has persisted to develop its own version. There have been rumors that MNKD is seeking a partnership since 2009, but nothing has materialized. MNKD is probably waiting for approval before becoming serious in negotiations. But investors must wonder if MNKD will be left hanging to dry as many big pharma companies will be reluctant to market another inhaled insulin.

Diabetic patients are a huge market and treatment is typically life long. This means that pharma/biotech companies are interested to capitalize making drugs for diabetes treatment.

According to the American Diabetes Association:

Afrezza is an inhaled insulin therapy for meal time control of blood sugar in patients with diabetes based on a novel dry powder form, Technosphere Insulin. MNKD must prove to investors and potential partners that it can succeed where Pfizer failed with Exubera. MNKD must demonstrate that Afrezza:

The There is a decreased incidence of weight gain and hypoglycemia with Afrezza. The lower risk of hypoglycemia (low blood glucose) can be attributed to the rapid decline in insulin levels. Afrezza also has a better tolerability profile than available forms of insulin.

PFE's Exubera

Exubera's inhaler was big and clunky. Patients would look ridiculous and arouse suspicion when using it. The Exubera inhaler worked similarly to an asthma inhaler. The patient needed actuation-breath coordination when using it. This required a learning curve and pharmacists and doctors to take time to teach patients. You know the design was bad when patients rather inject themselves then simply inhale.

MNKD's Afrezza

Afrezza's inhaler is a big upgrade over Exubera's. The Afreeza inhaler is small and discreet. Patients can easily carry it in a pocket or purse. The inhaler is breath actuated thereby getting rid of a large chunk of the learning curve and improving the precision and accuracy of dose delivery.

Afrezza's blockbuster potential lies in its costs. A report by Black et al. stated that Exubera's efficacy did not justify the extra cost. To be competitive, Afrezza must be similarly priced to injected forms of insulin or a price that justifies the convenience. Up to a 20% premium seems to be the consensus and if MNKD decides a higher price, expect insurers to not cover Afrezza and MNKD not to find a marketing partner or someone to buy it outright.

There was recent pullback in the stock price. The stock was trading at $8.17 at the time of writing. A FDA approval would definitely help the price. I believe the increase would be slight as investors are likely to worry about a possible bust and how big a market share it can grab onto. The major increase will follow a partnership announcement with a big pharma to help market and distribute Afrezza. This would happen a couple of weeks after FDA approval. The market potential for an inhaled insulin is huge and MNKD's marketcap will go through the roof.

If MNKD fails to win approval or is issued a Complete Response Letter, the price will begin to tank. The bottom will depend on what the FDA wants from MNKD; additional studies on safety or efficacy. MNKD at this point has nothing to fall back on. It's other drug candidates are in earlier stages of clinical trials or in the pre-clinical setting.

Diabetic patients are a huge market and treatment is typically life long. This means that pharma/biotech companies are interested to capitalize making drugs for diabetes treatment.

According to the American Diabetes Association:

"The national cost of diabetes in the U.S. in 2007 exceeds $174 billion. This estimate includes $116 billion in excess medical expenditures attributed to diabetes, as well as $58 billion in reduced national productivity. People with diagnosed diabetes, on average, have medical expenditures that are approximately 2.3 times higher than the expenditures would be in the absence of diabetes. Approximately $1 in $10 health care dollars is attributed to diabetes. Indirect costs include increased factors such as absenteeism, reduced productivity, and lost productive capacity due to early mortality."

Afrezza is an inhaled insulin therapy for meal time control of blood sugar in patients with diabetes based on a novel dry powder form, Technosphere Insulin. MNKD must prove to investors and potential partners that it can succeed where Pfizer failed with Exubera. MNKD must demonstrate that Afrezza:

- Superior to injectable forms of meal time insulin

- Patients are willing to use it. Patients find their information via the internet. They will surely come across Pfizer's letter to physician reporting possible lung cancer risk with Exubera although those patients who developed lung cancer were smokers and the results were not significant.

- Ease of use. Although it may appear that an inhaler is easy to use. Insulin is given is specific doses in international units (IU). The dose for meal time insulin depends on what is being eaten. Afrezza must make it easy for patients to calculate and obtain the correct dose.

- Reduced risk of low blood glucose after administration.

- Cost similar to injectable insulin formulations or the premium worth the convenience.

The There is a decreased incidence of weight gain and hypoglycemia with Afrezza. The lower risk of hypoglycemia (low blood glucose) can be attributed to the rapid decline in insulin levels. Afrezza also has a better tolerability profile than available forms of insulin.

PFE's Exubera

{kind=link}

Exubera's inhaler was big and clunky. Patients would look ridiculous and arouse suspicion when using it. The Exubera inhaler worked similarly to an asthma inhaler. The patient needed actuation-breath coordination when using it. This required a learning curve and pharmacists and doctors to take time to teach patients. You know the design was bad when patients rather inject themselves then simply inhale.

MNKD's Afrezza

{kind=link}

Afrezza's inhaler is a big upgrade over Exubera's. The Afreeza inhaler is small and discreet. Patients can easily carry it in a pocket or purse. The inhaler is breath actuated thereby getting rid of a large chunk of the learning curve and improving the precision and accuracy of dose delivery.

Afrezza's blockbuster potential lies in its costs. A report by Black et al. stated that Exubera's efficacy did not justify the extra cost. To be competitive, Afrezza must be similarly priced to injected forms of insulin or a price that justifies the convenience. Up to a 20% premium seems to be the consensus and if MNKD decides a higher price, expect insurers to not cover Afrezza and MNKD not to find a marketing partner or someone to buy it outright.

There was recent pullback in the stock price. The stock was trading at $8.17 at the time of writing. A FDA approval would definitely help the price. I believe the increase would be slight as investors are likely to worry about a possible bust and how big a market share it can grab onto. The major increase will follow a partnership announcement with a big pharma to help market and distribute Afrezza. This would happen a couple of weeks after FDA approval. The market potential for an inhaled insulin is huge and MNKD's marketcap will go through the roof.

If MNKD fails to win approval or is issued a Complete Response Letter, the price will begin to tank. The bottom will depend on what the FDA wants from MNKD; additional studies on safety or efficacy. MNKD at this point has nothing to fall back on. It's other drug candidates are in earlier stages of clinical trials or in the pre-clinical setting.

Subscribe to:

Posts (Atom)